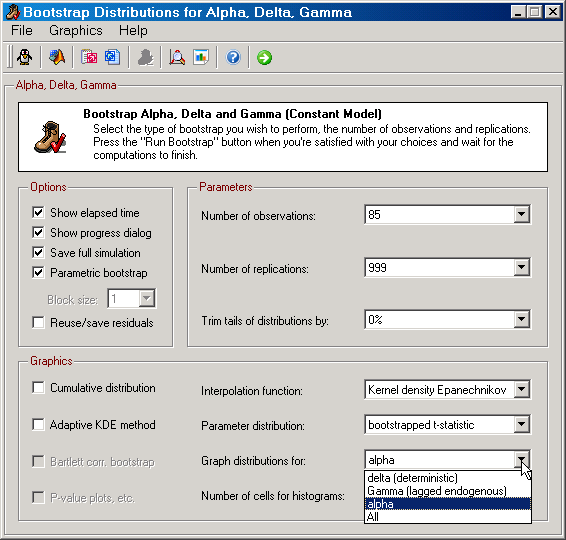

The bootstrapping features for α includes the LR test for over-identifying restrictions on α as well as empirical distributions for the free parameters of α (parameters on the cointegration relations), δ (parameters on deterministic variables), Γ (parameters on lagged first differences of the endogenous variables), Ψ (parameters on first differences of exogenous I(1) variables), and Φ (parameters on exogenous I(0) variables). The Parameters frame includes an optional "Trim tails of distributions" by a certain percentage drop-down control. The Graphics frame includes 2 additional features: the empirical parameter distribution to use in plots (t-value or parameter value based) and which parameter distributions to plot. All Common Features are supported.

|

Figure: The dialog for bootstrapping the distributions of the α, δ, Γ, Ψ, and Φ parameters. |