Estimation of the cointegrated VAR model under restrictions on β was discussed on the Restriction on (alpha,beta) page of the help file. Once estimation has completed, the results are presented on the Restriction on Beta dialog. From this dialog you can analyse some properties of the model subject to such restrictions as well as decide whether you want to use the new cointegration relations or not.

|

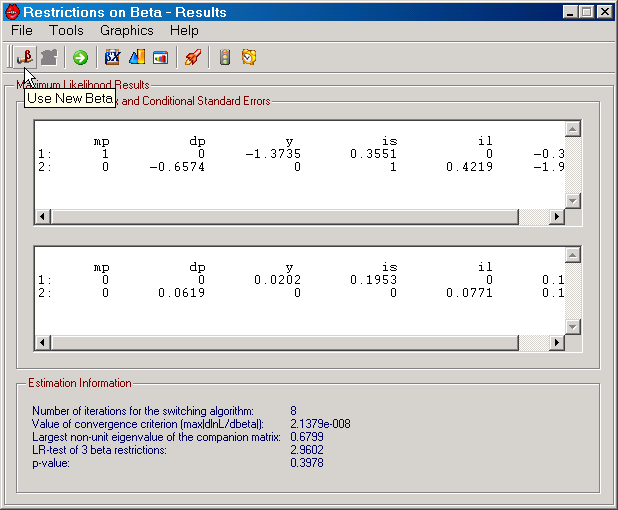

Figure: The Restrictions on Beta dialog in SVAR. |

The features that are presented on this dialog are shown in the Figure above. First of all, the estimated β vectors are given along with the estimated asymptotic conditional standard errors. The latter are computed as described by Johansen (1996), Theorem 13.4. For the β parameters that are restricted to a known value, the asymptotic conditional standard error does not exist (since the value is known), but is presented as 0 in the results frame for the conditional standard errors. Second, the number of iterations of the switching algorithm, the value of the convergence criterion (selected though the "Use gradient for restricted beta convergence" option on the Cointegration tab on the Preferences dialog), the largest non-unit eigenvalue of the companion matrix, the LR-test of any over-identifying restrictions, as well as the asymptotic p-value are given in the "Estimation Information" frame at the bottom of the dialog.

The Toolbar contains two buttons for selecting to:

| 1. | Use the new β (Use New Beta button), or |

| 2. | Not to use the new β (Recycle New Beta button). |

The current choice is given by the button that is disabled, i.e., greyed out. By default, the selection is to not use the new β (as shown in the Figure above). Hence, you must actively select to use the new β. These two selection functions are also available on the File Menu.

File Menu

| • | View Data: Allows you to view data in a file format that SVAR can read (see Data Input for details). |

| • | Save Cointegration Relations: Allows you to save the estimated cointegration relations in a text file. |

| • | Save Transitory Components: Allows you to save the transitory components (determined by a Beveridge-Nelson decomposition) in a text file. This feature requires that the model has at least one unit root. |

| • | Save Residuals: Allows you to save the estimated residuals in a text file. |

| • | Center Window: Centers the dialog window. |

| • | Use New Beta: Selects the restricted β estimate. Available on the Toolbar. |

| • | Recycle New Beta: Skips the restricted β estimate. Available on the Toolbar. |

| • | Continue: Return to the Restrictions on (alpha,beta) dialog. Available on the Toolbar. |

Tools Menu

| • | Serial Correlation: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | ARCH: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Normality: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Parameter Constancy: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Lag Order: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Weak Exogeneity: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Granger Causality: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Multi-Step Granger Causality: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Exclusion è |

| • | First Differences: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Common Cycles: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Deterministic Variables è |

| • | Exclusion: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Long Run: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Proportionality: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | C-Matrix: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Long Run GIRs: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Residual Analysis: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Short Run Dynamics: See the Tools Menu on the Cointegration Rank Tests dialog. |

| • | Distribution: See the Tools Menu on the Cointegration Rank Tests dialog. |

Graphics Menu

| • | Cointegration Relations: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Permanent and Transitory Components: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Residuals: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Fitted Terms: See the Graphics Menu on the Cointegration Rank Tests dialog. |

| • | Forecasting: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Forecast Variable Transformations: See the Graphics Menu on the Cointegration Rank Tests dialog. |

| • | Recursive Chow Test: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Recursive Fluctuation Test: See the Graphics Menu on the Cointegration Rank Tests dialog. Available on the Toolbar. |

| • | Generalized Impulse Responses: See the Graphics Menu on the Cointegration Rank Tests dialog. |

| • | Dummy Impulse Responses: See the Graphics Menu on the Cointegration Rank Tests dialog. |

| • | Log-likelihood and Beta: See the Graphics Menu on the Restrictions on (alpha,beta) dialog. |

| • | Eigenvalues of Companion Matrix: See the Graphics Menu on the Cointegration Rank Tests dialog. |

Help Menu

| • | Restrictions on Beta: Opens the help file on this page. |