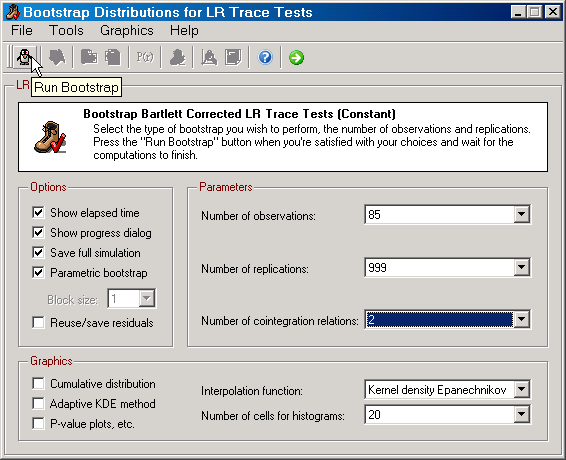

On this dialog you can bootstrap the LR trace tests. If you've selected to Bartlett correct the trace tests on the Cointegration tab on the Preferences dialog and you don't have any exogenous stochastic variables or deterministic variables beyond those that SVAR will setup itself, then this option will take effect. This also means that SVAR will run the bootstrap simulation for Bartlett corrected trace tests. Otherwise, it will do so for the standard LR trace tests.

|

Figure: The bootstrap LR Trace tests distributions dialog. |

In many instances the asymptotic distribution for the trace tests is not available in SVAR. If you have stochastic exogenous I(0) variables that are not treated as I(1) variables through accumulation (see Cointegration) or you've supplied one or more deterministic variables (dummies and whatnot), then the asymptotic distribution is taken as unknown. In case the only exogenous variables you have included in the model are treated as I(1), then the limiting distribution of the trace tests are included in the SVAR release for the models with either a restricted constant or with an unrestricted constant and a restricted linear trend. For the unrestricted constant and unrestricted linear trend models, the limiting distribution depends on nuisance parameters; see Harbo, Johansen, Nielsen and Rahbek (1998) for details. Still, from the bootstrap trace distribution dialog you can use bootstraps for computing p-values and other relevant statistics from the bootstrapped empirical distributions no matter which model you have.

One specific feature of the trace test bootstraps is that they make it possible to evaluate the power of the tests since only one rank can be true (among all possible cases). Moreover, it is possible to determine how often the selected rank at a given nominal level is less than the true rank. In that respect, the summary information on this dialog is the most comprehensive.