Bootstrapping the cointegration space tests means that 3 sets of tests related to α and β are subject to bootstrapping. All these tests are based on an exactly identified β matrix from the Johansen identification scheme. These tests are:

| • | Exclusion Tests: The exclusion statistic check if an endogenous or an exogenous I(1) variable has zero coefficients in β for all cointegration relations. The basic statistic is the LR test whose asymptotic distribution is the chi-squared with r degrees of freedom. See also the Cointegration Rank Tests page. |

| • | Stationarity Tests: The stationarity statistic checks if one of the cointegration vectors has zeroes on all variables but one endogenous (the stationary variable) and any constant or linear trend restricted to the cointegration space. The statistic is the LR whose asymptotic distribution is chi-squared with n-r+q1 degrees of freedom, where n is the number of endogenous variables, r the number of cointegration relations, and q1 the number of exogenous I(1) variables. See also the Cointegration Rank Tests page. |

| • | Test on Constant/Trend: The test on a constant or a linear trend depends on which deterministic variables selection you have made on the Parameters tab on the main program window. There you can choose between (i) Restricted Constant, (ii) Unrestricted Constant, (iii) Constant and Restricted Linear Trend, and (iv) Constant and Linear Trend. SVAR will here test: |

| • | (i) against (ii) if you have selected (ii) yielding n-r restrictions |

| • | (ii) against (iii) if you have selected (iii) yielding r restrictions, |

| • | (iii) against (iv) if you have selected (iv) yielding n-r, and |

| • | a zero constant against (i) if you have selected (i) yielding r restrictions. |

The test statistic is the LR whose asymptotic distribution is chi-squared with degrees of freedom equal to the number of restrictions. See also the Cointegration Rank Tests page.

|

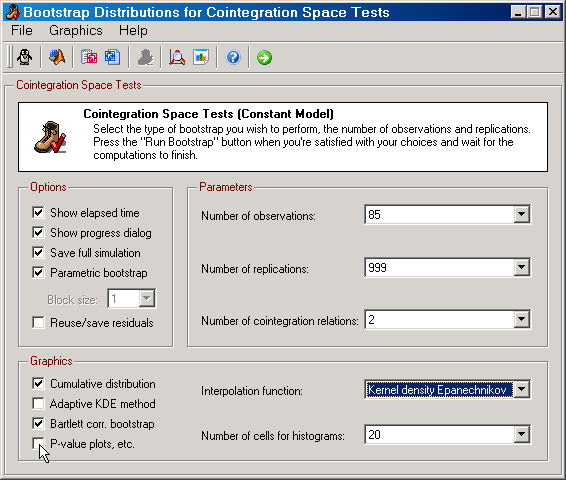

Figure: The dialog for bootstrapping the cointegration space tests. |